Assessment of Efforts to Provide Tax Relief to Eligible Taxpayers Impacted by the Ongoing Conflict in the State of Israel, Gaza, and the West Bank Why did we do this evaluation? In October 2023, terrorists launched an attack on the State of Israel which included the kidnapping and killing of Americans. Following the attack, the Treasury Department and the IRS issued a notice that grants tax relief to individuals and businesses affected by the terrorist attack. The IRS also posted a news release detailing taxpayer eligibility requirements that qualify for the postponement of various tax return filing and payment deadlines. When the IRS does not accurately identify all affected taxpayers in these instances, they may receive tax deficiency notices, which may place unnecessary stress on affected taxpayers. What did we find? The IRS proactively identified and marked tax accounts of likely affected taxpayers. Specifically, IRS management identified and proactively added freeze codes to 185,707 individual and 22,110 business tax accounts. In addition, the IRS made available well-established disaster relief processes for use by individuals and businesses who are affected by the terrorist attack to self-identify for tax relief. Read more of our findings: Assessment of Tax-Refund Related Products First, what are tax-refund related products? They are financial products for taxpayers expecting a tax refund. - Refund anticipation loans (known as RALs) are money borrowed by a taxpayer from a lender based on the taxpayer's anticipated tax refund. Once the IRS processes a taxpayer's tax return, the refund is sent to the lender to repay the loan. The benefit? Taxpayers can receive their refund quicker than the traditional IRS processing time of 21 days.

- Refund anticipation checks (known as RACs) direct a refund to a limited/special-purpose account at a financial institution. The benefit? The taxpayer doesn't have to pay tax prep fees upfront. The financial institution disburses fees for tax preparation and/or other services to the preparer and the balance of the refund to the taxpayer once they receive the refund.

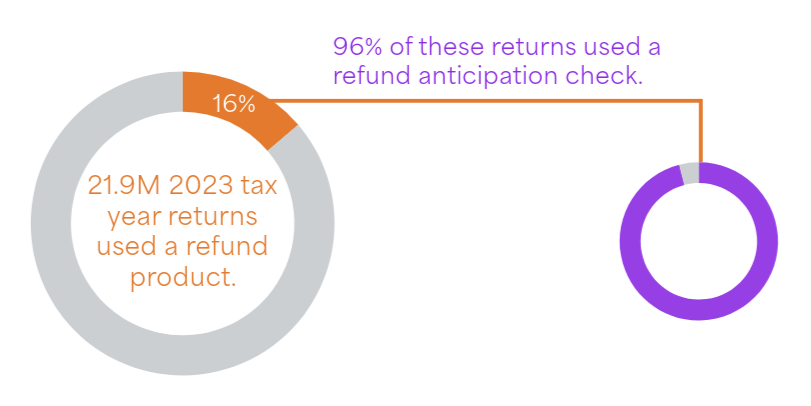

Why did we do this review? To assess refund advance and refund transfer products available to taxpayers, including their use, the cost and benefits of refund products to taxpayers, and an assessment of customer facing disclosures about fees. What did we find? We identified that 21.9 million out of 138 million (16%) tax year 2023 returns used a refund product. Most (96%) of these returns used a RAC.

We identified more than 53,700 tax return preparers associated with these products. However, 7 tax return preparer companies accounted for 77% of the total refund products.

We estimate taxpayers that used a RAC paid over $842 million in fees. The cost of RALs is unknown. We reviewed the websites of the top seven providers to review their disclosure of fees and found that while these providers are largely complying with guidance, not all information was clearly available for consumers. For more of our findings:

Having trouble viewing this email? View it as a Web page.

|

No comments:

Post a Comment