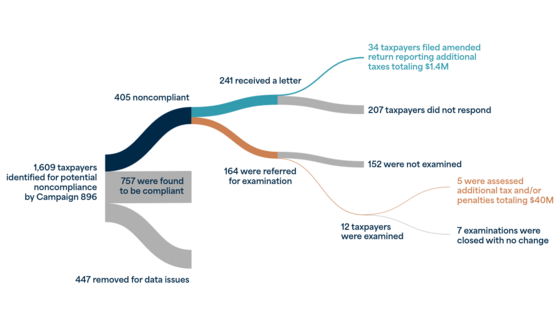

The IRS Has Not Successfully Addressed the Highest Balance Foreign Account Tax Compliance Act Nonfilers Why did we do this audit?The Foreign Account Tax Compliance Act (FATCA) was enacted to reduce the tax gap by identifying income held in foreign bank accounts. It promotes transparency and accountability for foreign assesses owned by U.S. taxpayers. Taxpayers with specified foreign financial assets that meet a certain dollar threshold should report this information to the IRS by filing Form 8938. Failure to file the form can result in penalties of up to $60,000. However, our previous reports showed that the IRS rarely enforces these penalties. The IRS established an Offshore Private Banking Campaign (Campaign 896) to address tax noncompliance related to taxpayers’ failure to file Form 8938 and information reporting associated with offshore banking accounts What did we find?Despite identifying hundreds of individual taxpayers with significant foreign bank account deposits who failed to file Forms 8938, Campaign 896 activity only resulted in a few taxpayer examinations and few nonfiling penalties. The campaign identified 405 taxpayers with significant foreign account balances who appeared to be noncompliant with their FATCA reporting requirements. The IRS used two methods to address the 405 noncompliant taxpayers: referral for examinations and letter issuance.

- 164 taxpayers (who had an average unreported foreign account balance of $1.3 billion) were referred for possible examination. However, only 12 of the 164 were examined, with five having $39.7 million in additional tax and $80,000 in penalties assessed.

- 241 noncompliant taxpayers (who had an average unreported account balance of $377 million) were sent a combination of 225 educational letters (requiring no response from the taxpayers) and 16 soft letters (requiring taxpayers to respond). None of the 241 taxpayers were assessed the initial $10,000 FATCA nonfiling penalty.

Campaign 896 Activity and Results  For more on what we found:

Having trouble viewing this email? View it as a Web page.

|

No comments:

Post a Comment